What is Sec 80G ?

Under this section, donor gets benefit of Tax Exemptions from his income, if he has donated to Organisation, having 80G Certificate.

Benefit to Donor

1. Its a charity and satisfy donor with sense of “giving”.

2. For Tax Exemption, 50% of the amount of donation will be exempt from Income Tax limiting to 10 % of Gross Income.

Benefit to Organisation

1. 80G approved NGOs get more donations.

2. Though it is not mandatory to have 80G certificate, many Funding Agency prefers 80G approved Organisations for funding.

Procedure :-

Application need to be filled in Form No 10G by Online mode only. Follow below steps to apply for 80G with the following documents.

Keep below documents/information ready

1. Copy of Registration Certificate.

2. Copy of Trust Deed / Society Deed/MOA.

3. Copy of PAN.

4. Copy of 12A Certificate or Acknowledgement of application of 12A.

5. Copy of last 3 years Audit Reports, if any.

6. Note on Activities for last 3 years, if any.

Notes :-

1. All the above copies must be self-attested by authorized person.

2. If certificate is in vernacular language, then get it translated in English and notarised it.

13 Steps for 80G Application

Step 1. Go to this website

https://www.incometaxindiaefiling.gov.in/home

Click on “Login”.

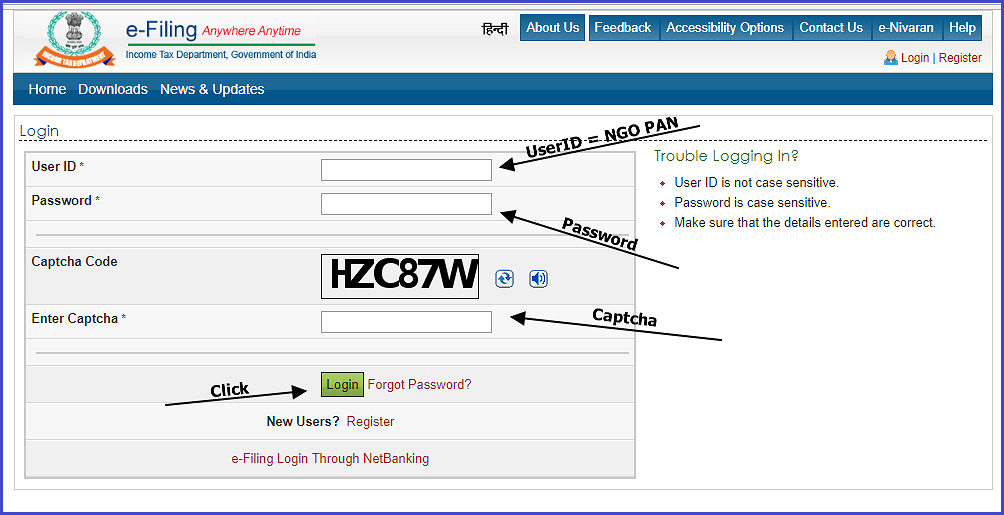

Step 2. Fill Login Details

Enter UserID = Organisation PAN.

Enter Password.

Enter Captcha.

Click “Login” .

Step 3. Go to “e-File”

Click on “Income Tax Forms”.

Step 4. Select Form Name = “Form No 10G …”

Step 5. Select Submission Mode = “Prepare and Submit Online”

Step 6. Fill General Information of Form

Click on tab “Form 10A”

Fill General Information – Name, Address, Email, Mobile etc..

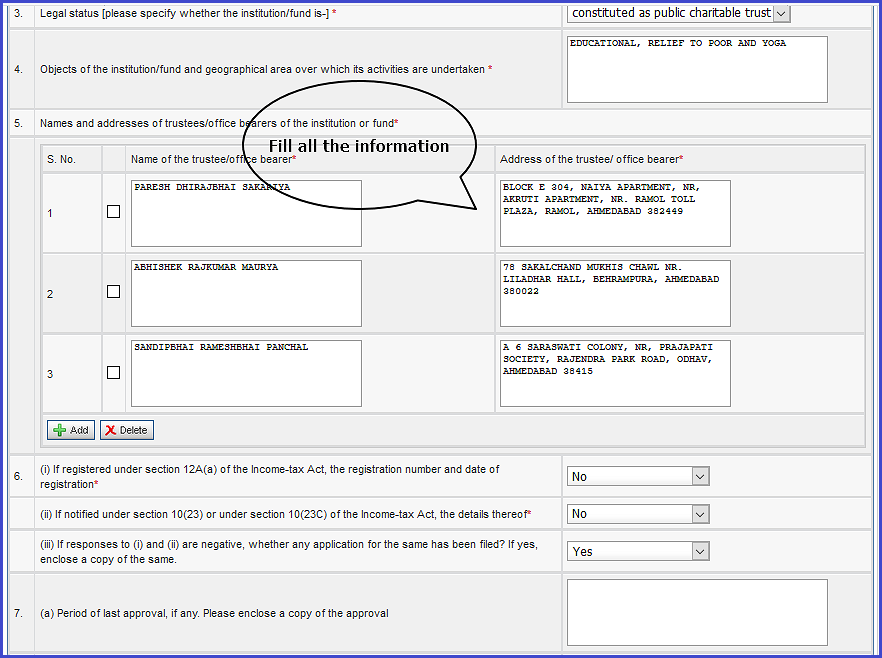

Step 7. Fill Trustee/Board Members Details

Step 8. Fill Applicable Details

Fill these other details whichever is applicable to your Organisation.

Step 9. Fill Detail of Signing Authority

Name, Address, Phone, Email etc..

Step 10. Preview the Form

Download draft form in PDF and check correctness of details.

Step 11. Upload Documents

Upload scan copies of relevant documents.

Click on “Submit” button in the bottom.

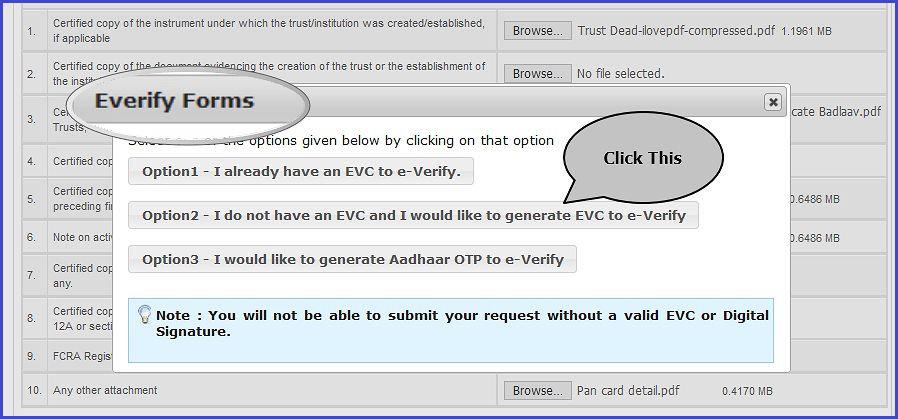

Step 12. E-Verification of Form

There are three options to e-verify this form.

1. If you have already generated EVC (E-Verification Code).

2. If you do not have EVC, click this, it will email you OTPs.

3. If you select AADHAR Option, OTP will be sent to Auhtorized

person Mobile linked with AADHAR.

Step 13. Acknowledgement

After verification as above, a Transaction ID has been provided. Note down that.

Also acknowledgement has been sent to given email address.

Take a print of it and keep it in file for future reference.

Time

Generally, within 15-30 days, a query raised by Assessing Officer asking for more documents or explanation.

Sometime, even Assessing Officer asked for personal visit by trustee or authorized person for explanation, if reqired.

Mostly within 2 to 3 months, Certificate of 80G has been issued.

Consequences

If, NGO do not have 80G certificate, donor can not get exemption

from tax from their Income and thus fund raising activity

certainly affected without 80G certificate.

Points related

Points related to Donation Receipts

1. Donation Receipt must contain – Date, Pre-printed serial number, Name and address of NGO, Name of Donor, Amount in figure and word, Mode of payment, Purpose of Donation, 80G certificate number and sign and seal.

2. It is advisable to have hardbounded receipt book with preprinted

serial number for good internal control system.

3. Trust can have multiple receipt books. But need to justify, why

it is necessary to have multiple receipt books.

4. It is advisable to issue receipts for each and every donation.

5. Also, keep PAN of Donor as a proof that it is not anonymous donation if asked by Assessing Officer.